Millions of people – children, adults, and seniors – need to access long-term services and supports (LTSS) as a result of disabling conditions and chronic illnesses.

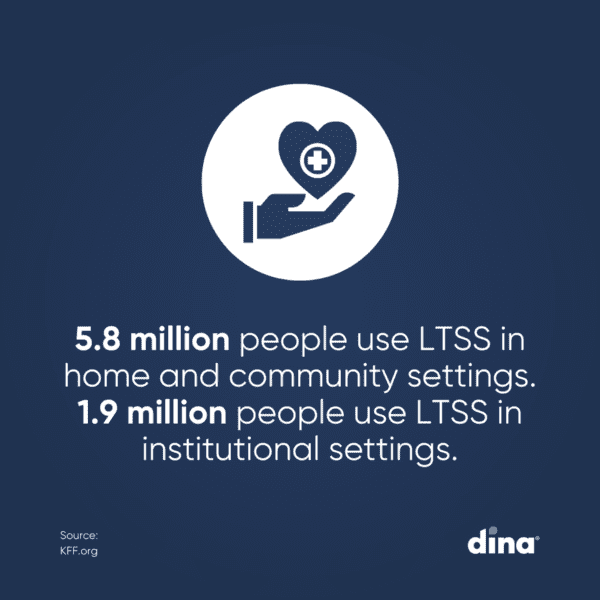

In 2020, an estimated 5.8 million people used LTSS delivered in home and community settings, and 1.9 million used LTSS delivered in institutional settings, according to CBO estimates.

Demographic trends suggest continued growth in the number of people who will need LTSS in the coming decades. Life expectancy remains relatively high, baby boomers continue to age into older adulthood, and advances in medical technology allow more people with chronic illnesses and disabling conditions to live longer and independently in the community.

This growth will continue to stress an industry already plagued with issues including staffing shortages, quality, and funding, without a clear resolution in sight.

Five Things to Know about LTSS

1. LTSS are expensive and not covered by Medicare

Medicare provides home health and skilled nursing facility care under specific circumstances, but the Medicare benefit is considered “post-acute” care and is generally not available for people needing services on an ongoing basis.

There are 8 million Medicare beneficiaries who meet the income, wealth, and health requirements for Medicaid and are enrolled in both programs (“dual eligibles”).

There are 8 million Medicare beneficiaries who meet the income, wealth, and health requirements for Medicaid and are enrolled in both programs (“dual eligibles”).

But for Medicaid-Medicare enrollees with full Medicaid benefits, Medicare is the primary payer for acute and post-acute care services and Medicaid covers ongoing LTSS. Medicaid plays a key role in affordability and access to LTSS for people who qualify, because LTSS costs may be difficult for people to afford when paying out-of-pocket.

In some cases, people only qualify for Medicaid after exhausting their savings on the costs of LTSS. The percentage of Medicare beneficiaries who are enrolled in Medicaid varies widely by state. Such variation reflects differences in state policy and in the income and wealth distribution of Medicare beneficiaries across the states.

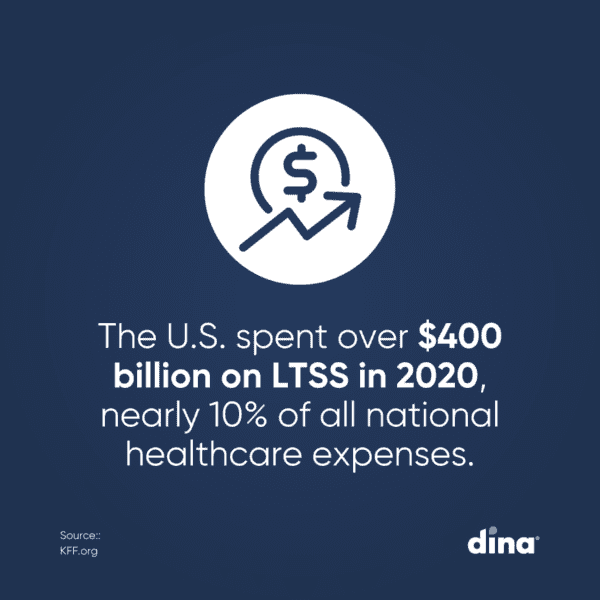

2. The U.S. spent over $400 billion on LTSS in 2020, nearly 10% of all national healthcare expenditures

In 2020, Medicaid paid 54% of the over $400 billion spent on LTSS in the U.S., people paid an additional 13% out-of-pocket, private insurance paid 8%, and other public and private payers paid the remaining 26%.

Home and community-based services (HCBS) include residential care facilities, Medicaid home health services, and Medicaid HCBS waiver services. Spending on those services was $245 billion and the remaining $157 billion was spent on institutional LTSS such as nursing facility care.

These totals exclude $86 billion in Medicare spending on post-acute care, and spending on home health that was paid out-of-pocket ($13 billion), by private health insurers ($16 billion), and by other public and private payers ($14 billion).

These totals exclude $86 billion in Medicare spending on post-acute care, and spending on home health that was paid out-of-pocket ($13 billion), by private health insurers ($16 billion), and by other public and private payers ($14 billion). Medicaid home health spending includes both acute care and LTSS, but it is likely that most home health is provided on an ongoing basis in the Medicaid program.

3. More than half of LTSS spending pays for home and community-based services, but there is variation across states

LTSS may be provided in various settings that are broadly categorized as institutional or non-institutional. Federal Medicaid statutes require states to cover institutional LTSS and home health, but the remainder of HCBS is optional.

Even without a mandate to cover HCBS, Medicaid LTSS spending has shifted from institutional to non-institutional settings over time. That shift reflects beneficiary preferences for receiving care in non-institutional settings and requirements for states to provide services in the least restrictive setting.

In 2019, in most states, at least half—and often much more than half—of LTSS spending was on HCBS. However, there is substantial state variation in the share of Medicaid LTSS expenditures that are spent on HCBS, ranging from 33% in Mississippi to 83% in Oregon.

Four states (Oregon, Minnesota, Arizona, and New Mexico) spent over 75% of their total Medicaid LTSS spending on HCBS, while 18 states spent under 50%

4. Most Medicaid LTSS spending is for people who are 65 or older or under age 65 with disabilities

In 2019, these groups comprised nearly 95% of fee-for-service LTSS spending but less than 25% of enrollment. Totals include spending on institutional and non-institutional care, but exclude spending paid for by managed care plans. Although the majority of LTSS is still paid for directly by states, the use of managed care to provide LTSS has increased over time.

5. States must provide institutional care and home health, but most HCBS are optional

Medicaid LTSS spending is shifting toward HCBS settings, but most major HCBS are optional for states to cover under Medicaid. The required HCBS are home health services; home health aide services; and medical supplies, equipment, and appliances suitable for use in the home. In 2020, about 734,500 people received mandatory home health services, which accounted for about 4.4% of Medicaid HCBS spending.

PACE Members Expect Quick Activation of Home-Based Services.

Does Your Plan Deliver?

See how easy it is to streamline access to medical and non-medical

home-centered benefits, support your centers, and quickly measure results.

What are LTSS?

LTSS encompasses a broad range of paid and unpaid medical and personal care services that assist with activities of daily living (such as eating, bathing, and dressing) and instrumental activities of daily living (such as preparing meals, managing medication, and housekeeping). They are provided to people who need such services because of aging, chronic illness, or disability, and include nursing facility care, adult daycare programs, home health aide services, personal care services, transportation, and supported employment.

These services may be provided over a period of several weeks, months, or years, depending on an individual’s health care coverage and level of need. They are designed to promote independence, enhance quality of life, and support individuals in their long-term care needs.

These services may be provided over a period of several weeks, months, or years, depending on an individual’s health care coverage and level of need. They are designed to promote independence, enhance quality of life, and support individuals in their long-term care needs.

Who Pays for LTSS?

Most people age 65 and older and many people under age 65 with disabilities have Medicare, but Medicare does not cover most LTSS. Medicaid is the primary payer for LTSS. To qualify for coverage of LTSS under Medicaid, people must meet state-specific eligibility requirements regarding their levels of income, wealth, and functional limitations. An unknown, but probably even larger number of people, used unpaid LTSS that is provided by family, friends, or neighbors.

Why are LTSS Important?

The goal of LTSS programs is to help people with functional limitations live safely, maintain quality of life, and maximize independence in their preferred setting. With access to care and supports, seniors and individuals with disabilities are better able to make choices about where they live and how they spend their time. Devastating and costly health incidents such as falls and malnutrition can often be prevented with proper services and supports such as personal assistance, home modifications, and home meal delivery programs. But without access to appropriate, high-quality care, people with functional limitations may suffer further health deterioration, which in turn causes unnecessary health care spending and unfavorable outcomes.

Meeting the Needs of an Aging Population

As the population ages and advances in medicine and technology enable people with serious disabilities to live longer, the number of people in need of LTSS is expected to grow.

As the population ages and advances in medicine and technology enable people with serious disabilities to live longer, the number of people in need of LTSS is expected to grow.

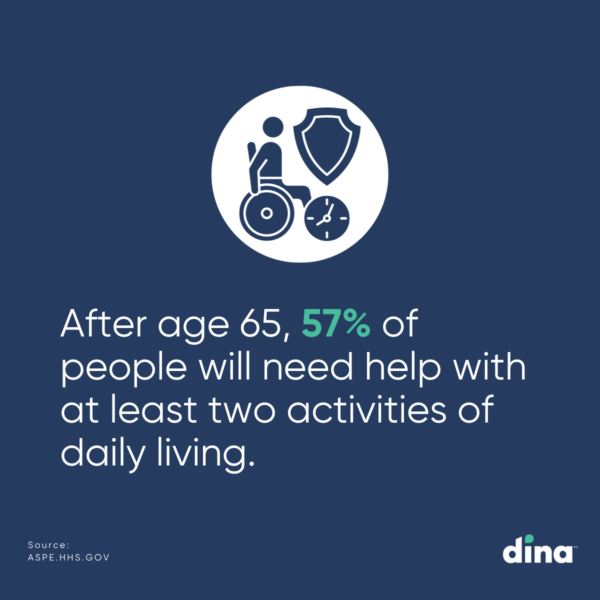

An HHS report found that after age 65, 57% of people would need help with at least two activities of daily living, 56% would use paid LTSS, and 39% would use some nursing home care. Expected rates of LTSS need and use are highest among people with lifetime earnings in the bottom income levels, who have the fewest resources to pay for such care.

Looking forward, there will likely be continued interest among policymakers in expanding the availability of LTSS and improving their quality, though identifying the resources to do so will be challenging.